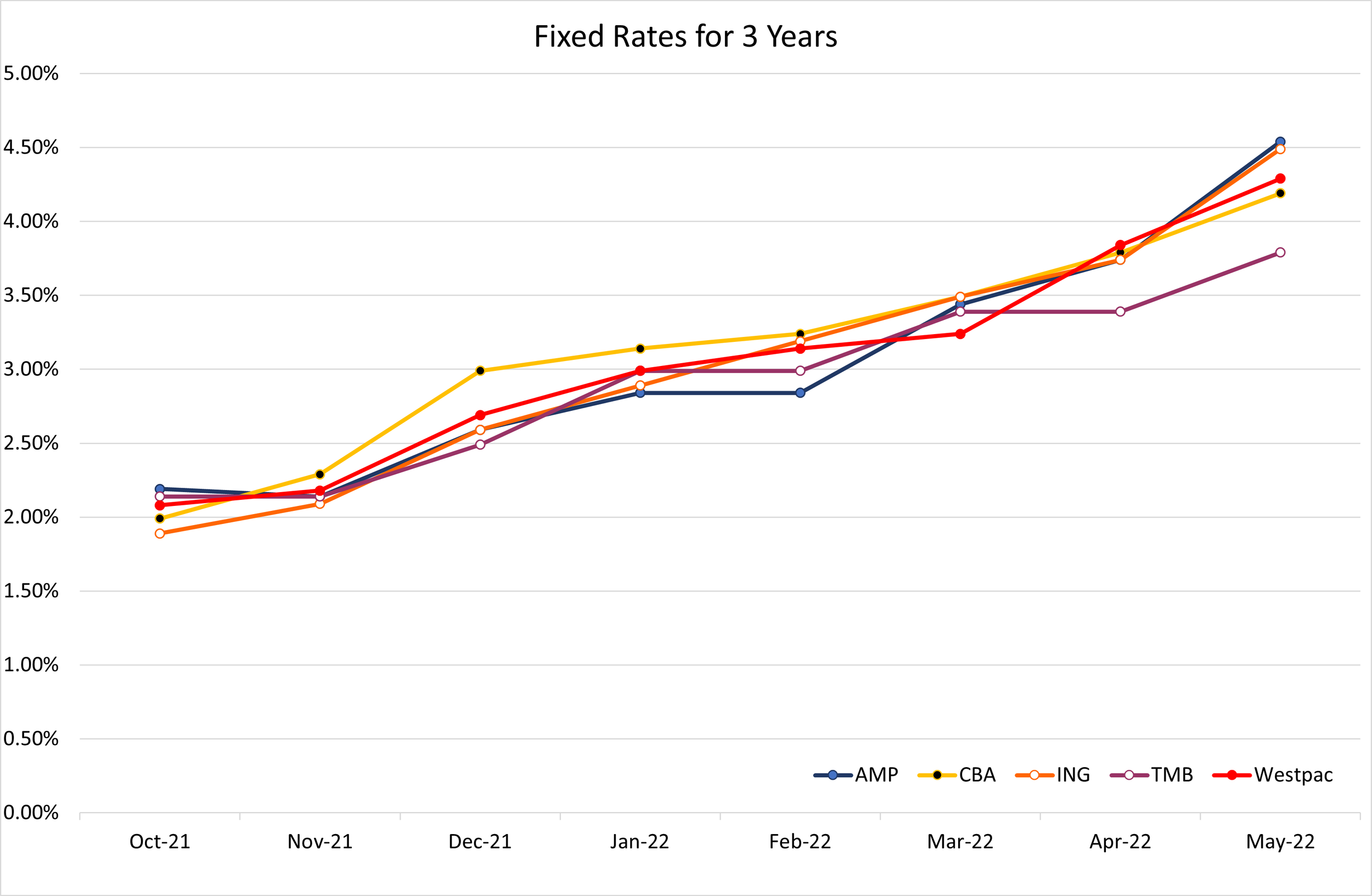

Impact on borrowers

Many borrowers locked their home and investment loan interest rates while they were at historically low levels in 2020 and 2021. This means that for many the impact of rising interest rates will not be felt for another 2 or 3 years. However, those borrowers need to get prepared for a potentially sharp increase in their loan repayments when their fixed term expires. To give you an idea of the scale of the impact:

For every 2% pa increase in rates P&I repayments will increase in percentage by approximately the number of years left on the loan – less 1%. For example, if when your fixed rate expires you have 26 years of your loan term remaining then your minimum monthly repayment will increase by about 25%.

In dollar terms minimum loan repayments will increase by between twelve and fourteen ($12-14) per month per $100,000 borrowed for every 25 bps increase in loan interest rate.

For example, if loan amount outstanding is $500,000 and interest rates increase by 1% pa then the minimum monthly repayment will increase by $260.

How do I prepare for this?

If you are in the market to purchase a property

There are a few things to bear in mind when rates are rising:

Set your household budget as if interest rates have already risen to 5.5% pa. This should inform the maximum loan you can contemplate and ultimately how much you can afford to pay for a property.

Do not be put off by higher fixed rates. Structure your loan in line with your own appetite for risk and your capacity to deal with increasing interest rates.

Do not “bet against the bank” with rates. They understand money markets much better than most individual borrowers, and will usually structure a premium into interest rates to cover off the increased risk they are taking.

When choosing your lender look beyond their initial interest rate for the loan. Ask your broker about each bank’s reputation for keeping rates low for existing customers as opposed to attracting new ones.

If your loan is currently fixed

Do you really know your household budget? In my experience most families (including mine!) do not always have a good handle on how much they are really spending. Go through your bank statements and add up all those small transactions to measure how much you are really spending.

Re-cast your household budget now. Calculate your likely loan repayments at 5.5% pa and start repaying that amount now to reduce your loan balance as much as possible. That way you will be “cash flow fit” for when rates do rise.

Set up a cash management strategy. Set your budget and savings goals and then direct your savings to your loan account and leave them there unless you encounter a real emergency. Using today’s technologies, it easy to set up an automated system that helps you to direct only your budget spending to the bank account you live from.

If you have a mortgage offset account, then operate it as a savings account. Your transaction / everyday account should be a different account, ideally with a different bank. If there is an ATM card linked to your offset account, put it in a drawer – you don’t need it!

Things to avoid doing

Convert your loan to interest-only repayments. If you’re having that much financial difficulty, then such a restructure is unlikely to be approved because it only helps you to worsen your financial position and leads to higher loan repayments later on.

Extend your loan term back to 30 years – this is another way of kicking the can down the road. It may be a reasonable solution in certain rare circumstances, where you are dealing with a short-term cash flow issue with a known resolution. But most people will be better off in the long term by addressing their fundamental cash flow challenge. Hard decisions made now lead to easier decisions in the future.

And remember that when rates return to the 5% level that this is more historically normal in Australia. Don’t feel hard done by – we have been living through extraordinary times and mortgage borrowers have been indirectly subsidised by the Federal government for 2 to 4 years to help maintain the economy. Those times are coming to an end.

If you need help in setting up a cash management strategy do not hesitate to contact my office for a consultation on how to go about it.

References

Janda, M. (2022) The cost of living is surging, so why will the RBA add to it by raising interest rates? ABC Business

Loanscape has today released its Borrowing Capacity Index for Q4/2024. It confirms the forecast trend that borrowing capacities of Australian individuals and families are recovering from their low levels which coincided with the last of the recent increases to borrowing rates initiated by the Reserve Bank of Australia.